A lessor is the party that owns or provides an asset and gives another party the right to use it under a lease. The lessor usually receives rent, lease payments, or other consideration from the lessee.

That definition is useful, but it is not enough for audit work. If the company you are auditing is the lessor, the key question is not only "who owns the asset?" It is "how do we prove the lease income, receivable, asset ownership, contract terms, and classification in Excel?"

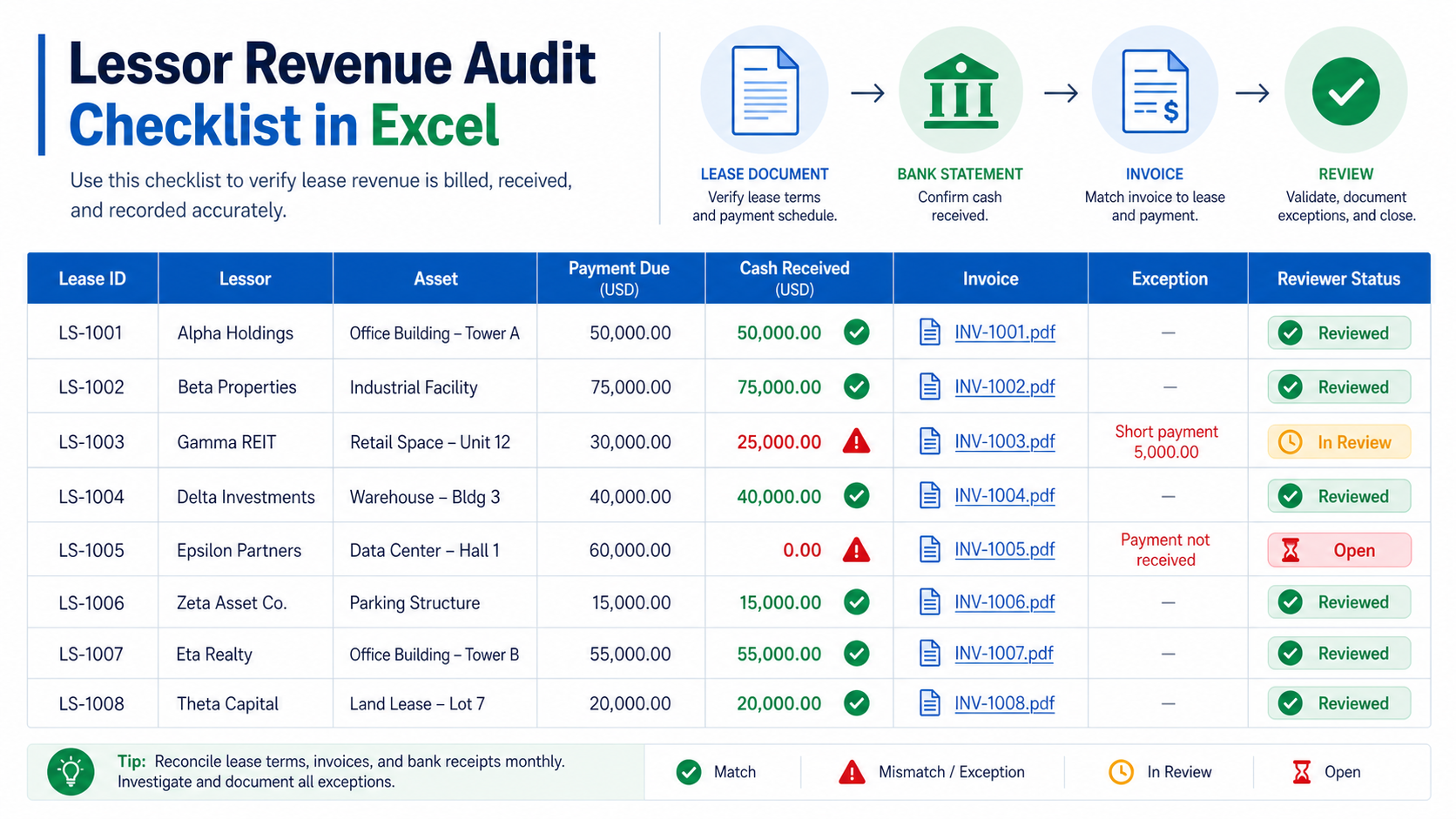

Auditing lessor contracts in Excel? Blast Audit helps teams extract lease terms from PDFs, match payments to schedules, and keep source evidence linked to the workbook. Start with Snip for source-linked evidence or Matching for document-to-cell reconciliation.

What Does Lessor Mean?

A lessor is the owner, landlord, finance company, or asset provider that grants another party the right to use an asset for a defined period. The party using the asset is the lessee.

Cornell's Legal Information Institute defines a lessor as the owner of property who contracts with a lessee to allow temporary possession through a lease: Cornell LII lessor definition.

In plain English:

| Term | Plain meaning | Common example | Audit focus |

|---|---|---|---|

| Lessor | Party that provides the leased asset | Landlord, fleet owner, equipment finance company | Lease revenue, receivables, asset ownership, classification |

| Lessee | Party that uses the leased asset | Office tenant, manufacturer, delivery company | Lease liability, payment schedule, ROU asset |

| Lease | Contract that grants usage rights for payment | Five-year office lease or vehicle lease | Contract terms, dates, options, payment clauses |

A landlord renting office space is a lessor. A bank or finance company leasing equipment is a lessor. A fleet provider leasing vans to a delivery business is a lessor.

If you need the other side of the contract, read Lessee Meaning: Definition & Audit Examples. If you need the side-by-side distinction, read Lessor vs Lessee.

Why Lessor Meaning Matters in Accounting

For a searcher, "lessor meaning" often starts as a vocabulary question. For an audit team, it quickly becomes a revenue, receivable, and asset classification question.

The lessor may need to show that it still owns the underlying asset, that lease income is complete, that receivables are collectible, and that lease classification is supported. Under lease standards, lessor accounting depends on the type of arrangement and whether the lease transfers substantially all risks and rewards or control economics to the lessee.

FASB's lease project page explains the broader lease accounting framework for Topic 842: FASB leases guidance. IAS Plus summarizes IFRS 16 and notes that lessor accounting remains substantially similar to the previous IAS 17 model, with operating leases and finance leases still relevant for lessors: IAS Plus IFRS 16 overview.

For auditors, the practical point is simple: when the company is the lessor, the workpaper should support the asset, the contract, the billing stream, the cash received, and the classification judgment.

The Audit Risk Behind the Definition

The main lessor audit risk is completeness of income. If a lessor has active leases that are missing from the lease register, revenue and receivables may be understated.

The second risk is collectibility. A lessor may record receivables from lessees who are late, disputed, or unlikely to pay. That creates valuation and allowance questions.

The third risk is classification. A contract may be treated as an operating lease when finance lease treatment is required, or the reverse. Classification can change revenue timing, balance sheet presentation, and disclosure.

The fourth risk is evidence quality. Even if the accounting is right, the audit file is weak if reviewers cannot trace Excel values back to contracts, invoices, cash receipts, or approved schedules.

This is where Blast Audit can out-position a broad document automation page. DataSnipper can compete on financial document automation across many document types. Blast Audit can make the lessor definition useful for the Excel audit workflow: extract the contract term, match the billing schedule, reconcile cash, and leave a reviewer-ready trail.

Real Examples of a Lessor

Example 1: Office Landlord

A property company owns an office building and leases one floor to a software company. The property company is the lessor. The software company is the lessee.

An auditor reviewing the lessor side may test:

- Whether the signed lease exists and is approved.

- Whether the rental rate agrees to the lease schedule.

- Whether escalation clauses are billed correctly.

- Whether rent receivable agrees to invoices and cash receipts.

- Whether lease incentives are recorded properly.

- Whether deposits and deferred income are classified correctly.

This work usually happens in Excel. The lease is a PDF, the rent roll is a spreadsheet, invoices may come from billing software, and receipts may come from bank statements. The risk is not one missing definition. The risk is a broken evidence chain.

Example 2: Equipment Finance Company

An equipment finance company owns a machine and leases it to a manufacturer for four years. The finance company is the lessor.

The auditor may need to inspect the equipment description, contract term, residual value, payment frequency, end-of-term option, and classification analysis. If the contract is scanned, OCR matters because the clauses are not searchable until the PDF text is recognized.

Blast Audit's OCR for Excel supports this kind of audit flow: import the document, make it searchable, and extract the evidence into the workbook.

Example 3: Vehicle Fleet Provider

A fleet provider leases 80 vans to a delivery business. The provider remains the lessor and receives monthly payments.

The audit challenge is population and payment matching. The reviewer may ask whether all vans are in the lease register, whether terminated vehicles were removed, whether new vehicles were added at the right date, and whether monthly billings match the contract.

Instead of checking each row manually, auditors can use document matching in Excel to compare schedules, invoices, and payment evidence.

What Auditors Usually Need From a Lessor Contract

When the company is the lessor, auditors usually need these fields:

| Contract field | Why it matters | Excel audit check |

|---|---|---|

| Lessor name | Confirms the reporting entity | Agree to entity list and contract header |

| Lessee name | Identifies counterparty and credit exposure | Agree to customer master and invoices |

| Asset description | Proves what is being leased | Agree to fixed asset register or lease register |

| Commencement date | Starts billing and accounting timeline | Recalculate first invoice and recognition date |

| Lease term | Drives classification and revenue schedule | Agree months, end date, and renewal assumptions |

| Payment amount | Drives income and receivables | Match to invoices and cash receipts |

| Escalation clauses | Changes future billing | Test step-ups or indexed increases |

| Residual value terms | Affects lessor economics | Inspect valuation and end-of-term assumptions |

| Purchase option | May affect classification | Inspect management conclusion |

| Security deposit | Affects liability or cash presentation | Agree to cash and contract terms |

The best workpaper does not just list these fields. It links them to the source clause.

Lessor Accounting Under ASC 842 and IFRS 16

Lease accounting is detailed, and this article is not accounting advice. But auditors can use a simple workflow when reviewing lessor arrangements:

- Confirm the company is the lessor.

- Identify the leased asset and ownership evidence.

- Determine whether the contract contains a lease.

- Extract term, payment, renewal, termination, and purchase option clauses.

- Review lease classification.

- Reconcile billing schedules to contract terms.

- Match invoices and cash receipts.

- Review receivables, deferred income, and disclosures.

The IFRS Foundation describes a lease as a contract that conveys the right to control the use of an identified asset for a period of time in exchange for consideration: IFRS Foundation agenda decision on lease definition.

That source matters for lessors too. If the contract does not provide the customer with control of an identified asset, it may be a service arrangement instead of a lease. The audit team should not rely only on the contract title.

What DataSnipper Covers vs What Blast Audit Can Own

DataSnipper is a strong competitor in financial document automation. Its site describes an audit and finance platform for collecting, extracting, cross-referencing, and verifying data: DataSnipper.

The competitor data in this brief explains why datasnipper.com can own broad informational SERPs: roughly 50K organic visits per month, domain authority 60/100, about 601 top-3 pages, and 3,494 tracked ranking keywords. Blast-audit.com is earlier: roughly 21 organic visits per month, domain authority 0/100, and no top-3 pages yet.

That gap argues for a narrow page. A generic lessor definition page answers "what does lessor mean?" Blast Audit should answer the next audit-specific question: "How do I test lessor revenue and contract evidence inside Excel?"

| Topic | Broad document automation angle | Blast Audit Excel audit angle | Why it matters |

|---|---|---|---|

| Definition | Explain lease parties | Map lessor role to audit procedures | Searcher gets a practical next step |

| Evidence extraction | Pull values from documents | Snip contract clauses into cells | Reviewer can trace each value |

| Revenue testing | Cross-reference documents | Match rent schedule, invoices, and cash in Excel | Income completeness is a key risk |

| Asset support | Process documents | Tie leased asset to fixed asset evidence | Lessor ownership must be supported |

| Review trail | Automate finance documents | Keep workbook-native source links | Audit teams live in Excel |

For bottom-funnel comparison, read DataSnipper vs Blast Audit. For a broader tool shortlist, read Best Audit Software for Excel.

Excel Audit Workflow for Lessor Contracts

Step 1: Build the lease population

Start with the lease register, rent roll, equipment schedule, customer list, or contract repository. The goal is to confirm that every active lessor contract is captured.

For a property lessor, compare rent rolls to leases and billing records. For an equipment lessor, compare asset records to active contracts.

Step 2: Extract the terms that drive billing

Capture commencement date, payment amount, frequency, escalation clauses, incentives, security deposits, renewal options, termination clauses, and purchase options.

With Snip, auditors can extract these terms from the PDF into Excel while preserving a source link.

Step 3: Match invoices and cash receipts

Lease income should agree to the contract, invoice, and cash receipt. If the lessor uses deferred billing, free rent periods, or step-up rent, the schedule should explain the timing.

The IRS also emphasizes recordkeeping for rental activity because records support financial statements, receipts, expenses, tax returns, and reported items if audited: IRS rental income and recordkeeping.

Step 4: Review exceptions

Exceptions should be visible in the workbook:

- Active contract with no invoice.

- Invoice with no cash receipt.

- Cash receipt with no lease schedule line.

- Escalation clause not reflected in billing.

- Expired lease still billed.

- New asset with no signed contract.

Related Reading

This page supports the long-tail lease cluster that Blast Audit can realistically build before chasing broad head terms where datasnipper.com has a 60-point domain authority advantage.

- For the user side of the lease, read Lessee Meaning.

- For the direct role comparison, read Lessor vs Lessee.

- For the accounting asset created on the lessee side, read Right-of-Use Asset.

- For the broader long-tail strategy, read DataSnipper vs Blast Audit.

FAQs About Lessor Meaning

What does lessor mean?

A lessor is the party that owns or provides an asset and allows another party, the lessee, to use it under a lease agreement.

Is a lessor the same as a landlord?

Often, yes. In a property lease, the landlord is usually the lessor. In equipment, vehicle, or software leases, lessor is the broader term.

What is the difference between a lessor and a lessee?

The lessor provides the asset and receives lease payments. The lessee uses the asset and usually makes the payments.

Does the lessor own the asset?

Usually yes. The lessor typically owns or controls the asset being leased, although legal structures can vary.

What should auditors test for a lessor?

Auditors usually test lease income completeness, receivables, asset ownership, contract terms, classification, invoices, cash receipts, and disclosures.

How can auditors test lessor contracts in Excel?

Auditors can import lease contracts, run OCR when needed, extract billing terms into Excel, match invoices to cash receipts, and keep source links for reviewer support.

Final Takeaway

"Lessor" means the party that provides the leased asset. For auditors, that definition points to a practical Excel workflow: prove the asset, extract the contract terms, test the revenue stream, match cash, and document the review trail.

DataSnipper can compete on broad financial document automation. Blast Audit can win the Excel-specific audit job behind the definition. Review Blast Audit pricing or start with Snip for source-linked lessor evidence.