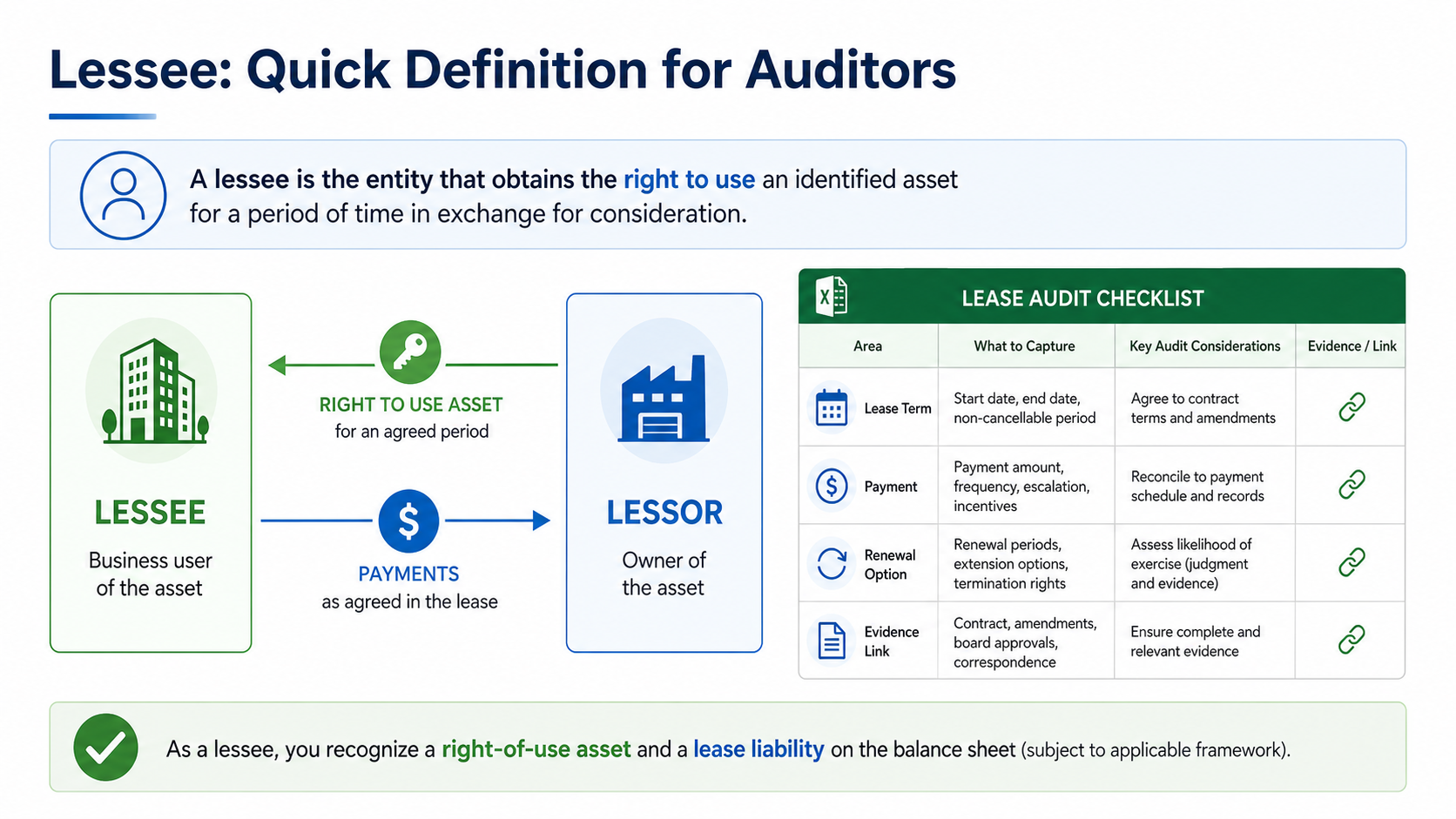

To define lessee in plain English: a lessee is the party that receives the right to use an asset under a lease. The lessee usually pays the lessor and follows the terms of the lease agreement.

That is the short answer. In audit work, the next question matters more: what does this role require the team to test in Excel?

This page is the quick definition spoke. For the deeper guide, examples, and lease accounting workflow, read Lessee Meaning: Definition & Audit Examples.

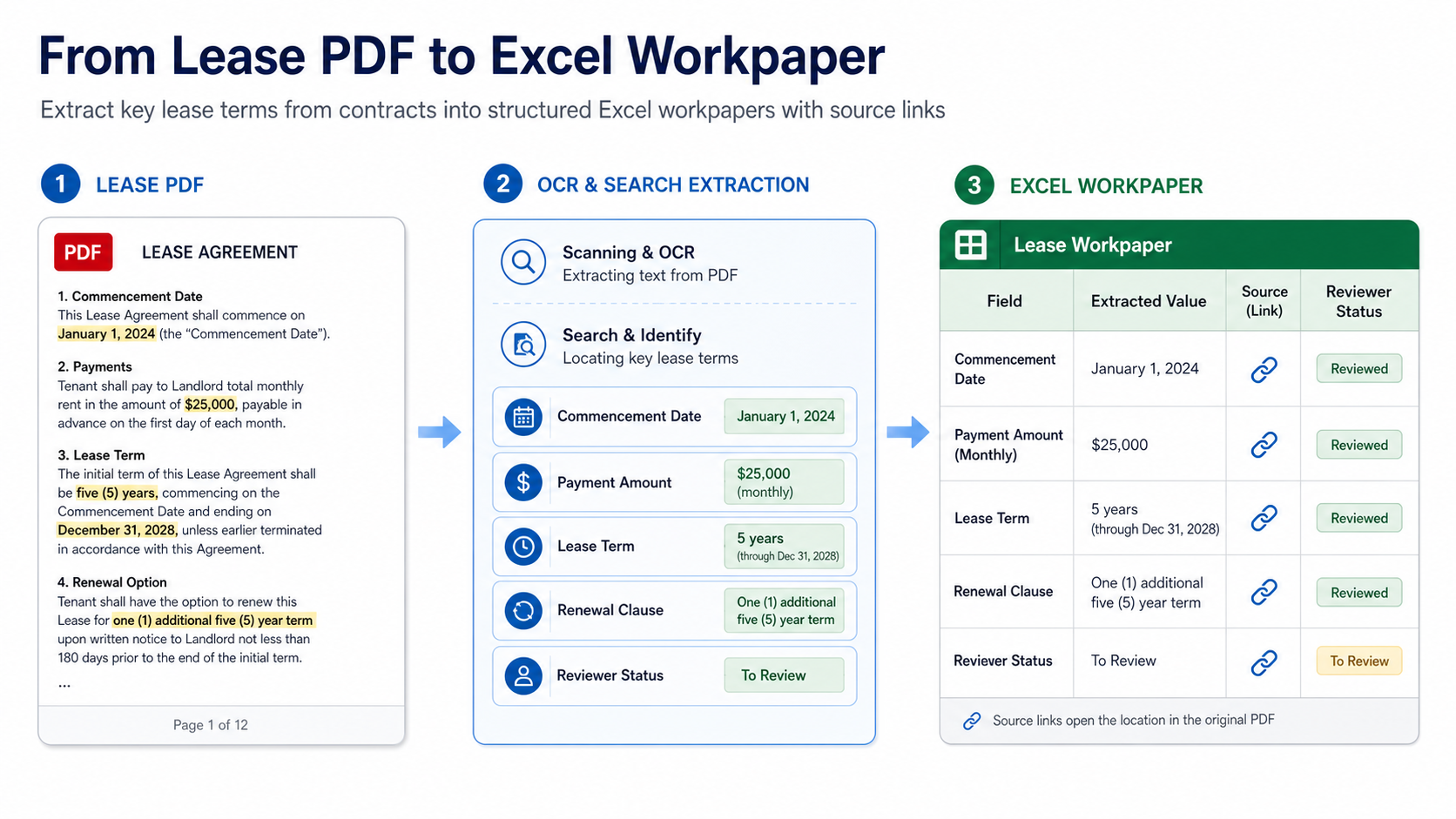

Testing lessee contracts in Excel? Blast Audit helps auditors extract lease terms from PDFs, link values to source evidence, and match payment schedules in the workbook. Start with OCR for searchable lease PDFs, Snip for source-linked terms, or Matching for payment evidence.

Define Lessee

A lessee is the person or business that uses an asset under a lease. The asset may be property, equipment, a vehicle, office space, software, or another resource.

The other party is the lessor. The lessor provides the asset and usually owns or controls it. Cornell's Legal Information Institute defines a lessor as the owner of property who contracts with a lessee to allow temporary possession through a lease: Cornell LII lessor definition.

| Word | Definition | Example |

|---|---|---|

| Lessee | Party using the leased asset | Company renting office space |

| Lessor | Party providing the leased asset | Landlord or equipment owner |

| Lease | Contract granting the use right | Five-year office lease |

The lessee is not usually the owner. The lessee has the right to use the asset for the lease term, subject to the contract.

Why Auditors Care About the Definition

The word "lessee" tells auditors which side of the contract they are testing. If the audited company is the lessee, the team usually reviews lease liabilities, right-of-use assets, payment schedules, and source support.

FASB explains that leases create rights and obligations that can require recognition of assets and liabilities for leases over 12 months under Topic 842: FASB leases guidance.

IAS Plus summarizes IFRS 16 as a single lessee accounting model requiring lessees to recognize a right-of-use asset and lease liability: IAS Plus IFRS 16 overview.

The audit implication is clear: defining the party is not just vocabulary. It points to the evidence that belongs in the workpaper.

Common Lessee Examples

Office tenant

A business signs a five-year office lease. The landlord provides the space. The business uses the space and pays rent.

The business is the lessee. The auditor may inspect the signed lease, commencement date, payment schedule, renewal option, and rent payments.

Equipment user

A manufacturer leases a machine from an equipment finance company. The manufacturer uses the machine and makes monthly payments.

The manufacturer is the lessee. The auditor may extract asset description, lease term, payment amount, residual value terms, and end-of-term options.

Vehicle fleet customer

A delivery company leases vans from a fleet provider. The fleet provider owns the vehicles. The delivery company uses them in operations.

The delivery company is the lessee. The audit team may test whether all vehicles are included, whether terminated vehicles were removed, and whether payments match the general ledger.

Lessee vs Lessor

The easiest way to remember the distinction is this:

- The lessee uses the asset.

- The lessor provides the asset.

- The lease sets the terms.

Read Lessor vs Lessee for the full comparison and Lessor Meaning for the owner/provider side.

What DataSnipper Covers vs What Blast Audit Can Own

DataSnipper is positioned around financial document automation. Its site describes a platform for collecting, extracting, cross-referencing, and verifying data: DataSnipper.

The competitor data in this brief shows why broad head terms are hard: datasnipper.com has roughly 50K organic visits per month, domain authority 60/100, about 601 top-3 pages, and 3,494 tracked keywords. Blast-audit.com has roughly 21 organic visits per month, domain authority 0/100, and no top-3 pages yet.

That is why this page stays narrow. It answers "define lessee" quickly, then moves into the Excel audit job that Blast Audit can own.

| Searcher need | Generic definition page | Blast Audit angle |

|---|---|---|

| Quick meaning | Define the term | Define it in the first sentence |

| Role distinction | Explain lessor vs lessee | Link role to audit procedures |

| Evidence | Mention lease agreement | Extract contract terms into Excel |

| Review | Not usually covered | Source-linked cells and exception review |

| Next step | Keep reading | Test the lease with OCR, Snip, and Matching |

Excel Checks After You Define Lessee

Once you know the company is the lessee, the audit work usually follows a predictable path.

1. Confirm the contract contains a lease

The IFRS Foundation describes a lease as a contract that conveys the right to control the use of an identified asset for a period of time in exchange for consideration: IFRS Foundation lease definition agenda decision.

That matters because a service contract can mention assets without creating a lease.

2. Extract the key contract terms

Auditors usually capture commencement date, lease term, payment amount, renewal options, termination rights, incentives, purchase options, and asset description.

With Snip, these values can be placed into Excel with source links.

3. Match payments to the schedule

Lease payments should agree to the contract, lease schedule, and general ledger. Differences should be visible as exceptions, not buried in folders.

4. Keep evidence reviewable

A reviewer should be able to click from an Excel cell to the supporting clause or document.

FAQ: Define Lessee

What is the definition of lessee?

A lessee is the party that receives the right to use an asset under a lease agreement.

Is a lessee a tenant?

Often yes. In property leases, a tenant is usually the lessee. Lessee is the broader term used across property, equipment, vehicle, and other asset leases.

Who is the lessor?

The lessor is the party that provides or owns the leased asset and receives payment from the lessee.

Does the lessee own the asset?

Usually no. The lessee has the right to use the asset during the lease term, while the lessor typically retains ownership.

What should auditors test after identifying the lessee?

Auditors usually test lease completeness, contract terms, payment schedules, right-of-use assets, lease liabilities, and source evidence.

Final Takeaway

To define lessee: it is the party that uses an asset under a lease. For audit teams, that definition should lead directly to Excel evidence: extract the contract terms, match the payment schedule, and keep the reviewer linked to the source.

For the full hub, read Lessee Meaning. To test lessee evidence in Excel, review Blast Audit pricing or start with Snip.